Firstrade Receives Accolades From Kiplinger’s, NerdWallet, and Stockbrokers.com!

OK, we’ll admit it. We’re human. We like to hear good things about us. Especially from prestigious and influential organizations covering our industry on a daily basis, such as Kiplinger’s Personal Finance, Stockbrokers.com and Nerdwallet.

But what’s most important is that these honors reflect the value and high-quality services our customers have come to expect from Firstrade.

OK, we’ll admit it. We’re human. We like to hear good things about us. Especially from prestigious and influential organizations covering our industry on a daily basis, such as Kiplinger’s Personal Finance, Stockbrokers.com and Nerdwallet.

But what’s most important is that these honors reflect the value and high-quality services our customers have come to expect from Firstrade.

Here’s a quick rundown:

Firstrade was ranked as a best broker for active traders, the number one brokerage for ETFs and for best commissions and fees by Kiplinger’s Personal Finance Best Online Brokers of 2019.

NerdWallet gave five stars to Firstrade, citing us as the best online broker for beginners, stock trading, IRAs and Roth IRAs, options and day trading.

Firstrade was awarded 5 stars for ease of use and 4.5 stars for commissions and fees by Stockbrokers.com.

We’re proud to provide our customers with the best trading tools, no commission trading and advanced research to help them make informed decisions and trade easier. We strive every day to improve the customer experience at Firstrade.

Stay tuned for more exciting news in 2020.

Why Infrastructure Upgrades Improve Your Trading Experience

Ok, so infrastructure is not the sexiest of topics. But guess what? Our society and economy could not survive without infrastructure in place. This of course includes the global financial system as well.

Ok, so infrastructure is not the sexiest of topics. But guess what? Our society and economy could not survive without infrastructure in place. This of course includes the global financial system as well.

Here’s a good definition we found from Market Business News: “Infrastructure refers to the basic systems and services that a country or organization needs in order to function properly. For a whole nation, it includes all the physical systems such as the road and railway networks, utilities, sewage, water, telephone lines and cell towers, air control towers, bridges, etc., plus services including law enforcement, emergency services, healthcare, financial services, education, etc.”

Now you know, but what does this have to do with investing at Firstrade you ask? Well, simply put, as a self-directed investment firm, we continually need to upgrade our infrastructure and IT systems to keep providing you with the best possible tools and resources to enhance your trading experience today and for the future. That’s why in the past year alone, we have doubled our investment in the core infrastructure.

Here’s what we’ve just done:

Completed a comprehensive infrastructure and technology upgrade of all our trading platforms and security systems. This initiative was undertaken to provide the best possible trading experience for our customers to maximize speed, execution and security.

The initial phase of the enterprise infrastructure project has been completed with the latest multi-core processors and a high-performance network storage system that’s based on 3D-NAND flash technology.

The new platform can perform up to three times faster than Firstrade’s previous version, delivering up to 300,000 I/O per second. This upgrade in speed can make the critical difference in whether a trade is successful or not and can help achieve real cost savings as well.

We’re testing multi-cloud system architecture to provide increased availability of the best cloud services.

Firstrade has long recognized that the speed and pace of trading in today’s financial markets have required the company to be consistently ahead of the curve in developing and providing leading-edge technologies. Our recent growth has been coupled with the significant investment we’ve made in technology.

We’re proud to be leading the way of our industry, but we’ll never rest on our laurels—more good news to come!

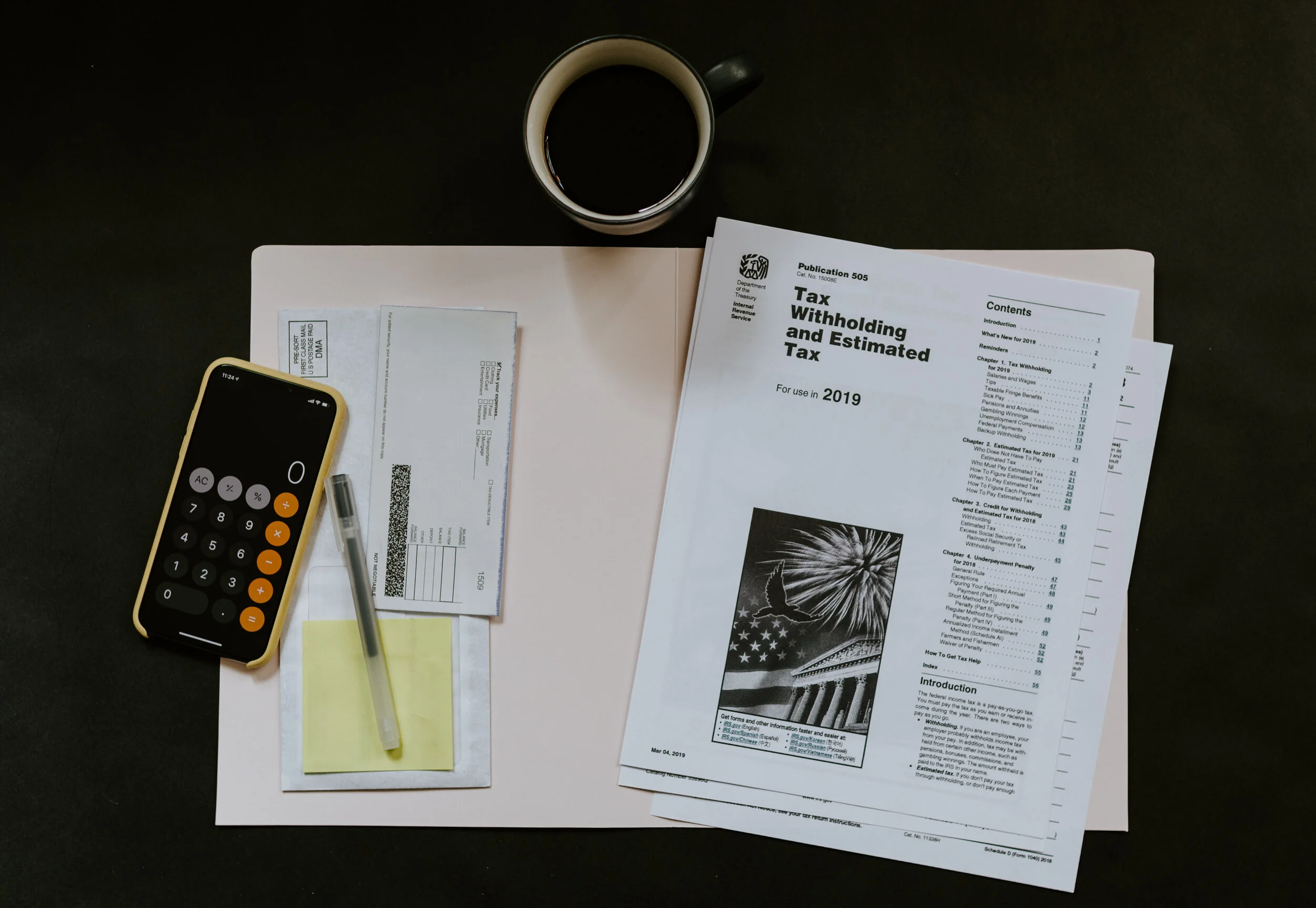

How to Save on Your 2019 Taxes

Investors know that a great portfolio requires strategic planning and consideration of economic factors that would impact your investments. So, it’s not unusual to think about how 2019 tax changes could affect your investment decisions as you look ahead to preparing to file your 2019 taxes.

Here are among the things you should be thinking about before the end of the year:

Investors know that a great portfolio requires strategic planning and consideration of economic factors that would impact your investments. So, it’s not unusual to think about how 2019 tax changes could affect your investment decisions as you look ahead to preparing to file your 2019 taxes.

Here are among the things you should be thinking about before the end of the year:

1. Contribute the maximum to your IRA

You can contribute as much as $6,000 to an IRA, up $500 from 2018. If you’re age 50 or older, you can make an additional $1,000 contribution.

2. Defer some income if you can

You only pay taxes on the income you receive during a given year. So, you can put off paying some taxes by deferring some income. While this may be difficult for salaried employees, consider deferring some income until next year. Perhaps you can defer your annual bonus, for instance. If you’re self-employed, it may be easier to delay payments until 2020. You may want to consult your accountant, however, because this only makes sense if you’re going to stay in the same or lower tax bracket next year.

3. Think about more deductions you can take

Here are some itemized deductions worth paying attention to:

Make your charitable donations by December 31, 2019 because charitable donations are deductible, and the cash donation limit is 60% of adjusted gross income (AGI).

State and local income taxes, property taxes, and real estate taxes are capped at $10,000.

The mortgage interest deduction is a tax deduction for mortgage interest paid on the first $1 million of mortgage debt. Homeowners who bought houses after Dec. 15, 2017, can deduct interest on the first $750,000 of the mortgage.

Medical expenses more than 10% of adjusted gross income (AGI) can be deducted.

No miscellaneous itemized deductions are allowed.

4. Contribute more to your flexible spending account (FSAs)

If your employer offers a health care FSA, take advantage of the increase in contribution limits. Your employer dictates what you can contribute, but the IRS maximum for 2019 is $2,700. Contribution limits for dependent care FSAs, remains at $2,500 for individuals and $5,000 for married couples or individual heads of household.

5. Consider “loss harvesting”

You may want to consider selling some stocks in your portfolio to realize losses, which can then offset any capital gains to reduce your overall tax burden. Losses will offset gains dollar for dollar so this could be a winning strategy for you.

6. Save on taxes with your health savings account (HSA)

The maximum amount you can contribute to an HSA for 2019 is $3,500 for an individual and $7,000 for a family. If you’re age 55 or over, you can contribute an extra $1,000.

7. You may qualify for the child tax credit

Kids are great, especially since the child tax credit could even be paid back as a tax refund. And, did you know that tax credits reduce your taxable income?

You may be eligible for a tax credit of up to $2,000 per dependent child age 16 and younger, if your household income is below $200,000 for single filers or $400,000 for joint filers. If your child is 17–24, you may still qualify for a credit of up to $500.

8. Beware the “kiddie tax”

A child’s investment income above $2,200 is taxed at the same rate as trusts and estates, which are usually higher than individual tax rates, so you may want to stay under that amount.

9. Alternative minimum tax (AMT) exemption could impact investment decisions

For 2019, the AMT exemptions are $71,700 for single filers, $111,700 for married taxpayers filing jointly, and $55,850 for married taxpayers filing separately. The phase-out thresholds are $1,020,600 for married taxpayers filing a joint return and $510,300 for all other taxpayers.

10. Give More, Save More on Estate Taxes

The unified estate and gift tax exemption is now $11.4 million for 2019. It’s higher than last year, but will expire at the end of 2025.

The gift tax exemption, which allows you to “gift” investments to family members, remains at $15,000 per recipient.

Big Changes Ahead for Saving for Retirement

Who says Washington can’t agree on anything?

With bipartisan support, Congress just passed and the President signed the SECURE Act, legislation that provides significant changes and incentives to further help Americans save for retirement. Most of the provisions will take effect on January 1, 2020.

So, what does this mean for your IRA and 401(k)? Among its major features, the SECURE Act:

Who says Washington can’t agree on anything?

With bipartisan support, Congress just passed and the President signed the SECURE Act, legislation that provides significant changes and incentives to further help Americans save for retirement. Most of the provisions will take effect on January 1, 2020.

So, what does this mean for your IRA and 401(k)? Among its major features, the SECURE Act:

Removes the maximum age limit for making contributions to traditional individual retirement accounts (right now, that’s 70½).

Makes it easier for small businesses to band together to offer 401(k) plans and offers tax credits to those firms that do.

Raises the age to 72, up from 70½, when people need to start taking required minimum distributions from certain retirement accounts.

Encourages annuities in 401(k) plans by eliminating companies’ fear of legal liability if the annuity provider fails or otherwise doesn’t deliver.

Allows for younger investors to use up to $10,000 of 529 plans to pay off student debt

Allows small businesses to participate in multi-employer 401(k) plans and receive tax credits for implementing automatic enrollment

Lets part-time workers become eligible for retirement benefits, depending on how many hours they’ve worked in a given year.

With many Americans falling woefully short in saving for retirement, these new measures will hopefully encourage people to save more in the years ahead.

What are you waiting for? Check out Firstrade’s retirement accounts.

The Tax Benefits of Custodial Accounts For Your Kids

To start saving for your child’s education or building that nest egg with a Firstrade custodial account. Firstrade makes it easy to open and manage with no custodian income limits or minimum deposit requirements.

What exactly is a custodial account you ask?

To start saving for your child’s education or building that nest egg with a Firstrade custodial account. Firstrade makes it easy to open and manage with no custodian income limits or minimum deposit requirements.

What exactly is a custodial account you ask?

It’s an investment account set up for a minor under the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA) based upon your state of residence. So unlike popular education accounts such as a 529 plan, you don’t have to be 18 years old or older to own them.

For that up-and-coming financial genius in your life, a custodial account is set up for a minor with money that is gifted to the child. The assets held in the account are owned by the minor under his or her name and social security number. And, the money can be used for any purpose, not just tuition, as long as it’s legally used for the benefit of the child.

The account is administrated by a custodian (usually a parent), who will manage the account for the minor’s benefit until he or she reaches the age of majority (18 or 21 depending on the state).

For the parent, a custodial account not only lets you manage your child’s assets, it provides a gift tax advantage (up to the maximum contribution allowed) and the flexibility to invest in any combination of investment products. Here’s how:

You can contribute up to $15,000 per person annually.

The first $1,050 in earnings is tax-free, the next $1,050 of earnings is taxed at the child's tax rate, and the earnings over $2,100 is taxed at the adult's tax rate.

You can invest in stocks, ETFs, mutual funds, bonds, and up to level 2 options trading.

You can withdraw the money for any purpose without time restrictions, as long as it’s for the benefit of the minor.

When the maximum allowed contribution exceeds $15,000, a gift tax could be incurred.

To enroll and learn more about a Firstrade custodial account, go here.