Not That Sexy, But Very Popular Nonetheless

OK, they may be boring but they’re a great long-term investment. Of course, we’re talking about mutual funds. We make it easy to invest in mutual funds—we’re the only online broker that has zero commission for all our mutual funds transactions! And, we support more than 4,000 no transaction fee funds, more than 10,000 no-load funds and 4,000 load funds.

OK, they may be boring but they’re a great long-term investment. Of course, we’re talking about mutual funds. We make it easy to invest in mutual funds—we’re the only online broker that has zero commission for all our mutual funds transactions! And, we support more than 4,000 no transaction fee funds, more than 10,000 no-load funds and 4,000 load funds.

Let’s take a step back for a moment. What are mutual funds and what makes them so appealing for investors?

Mutual funds are investments that pool your money with other investors to invest in stocks, bonds, and other securities. Each investor owns shares, which represent a portion of the holdings of the fund. Through a mutual fund, you can invest in many different underlying assets in one purchase.

Simply put, they’re a great way to diversify your portfolio, diversify your holdings within a particular sector, and create a professionally managed, low maintenance portfolio with low minimum investments. Like investing in the stock market in general, mutual funds also offer the liquidity to buy or sell at your own discretion.

And, you have your choice of sectors, levels of risk, investment types and more. Why put your eggs in one basket when you can fully diversify with a mutual fund? And, the beauty is that professional money managers are doing all the heavy lifting for you—it’s their job to develop an optimally balanced portfolio for you, always keeping diversification in mind.

But with so many choices, it may seem a little daunting to decide which mutual funds may be best for you. Still, there are steps you should take to determine what approach you should take.

Ask yourself what return you would like to make and the risk level you are willing to tolerate.

Do some research and have a good understanding of the fund that you are buying.

You can find information about a fund's goals, strategy, performance, management, and fee structure in its prospectus. Compare performance over time and in different economic and market environments.

There may be certain industry sectors that are of particular interest to you, such as technology or energy, where you may want to invest.

A fund manager's experience and record, the fund's level of consistency, and its major investment holdings are other important factors to consider.

Investors can also find information and ratings of mutual funds in various outlets such as Morningstar, Forbes, Value Line and Barron's.

To learn more about investing in mutual funds at Firstrade, visit here.

Your Child’s Education Can be Expensive, Duh

In our last blog, we discussed custodial accounts, which can be an effective way for families to save for their children’s education. Here’s another idea to consider—a Coverdell Education Savings Account (CESAs), formerly known as an Education IRA.

In our last blog, we discussed custodial accounts, which can be an effective way for families to save for their children’s education. Here’s another idea to consider—a Coverdell Education Savings Account (CESAs), formerly known as an Education IRA.

With college costs increasing at twice the rate of inflation, it’s important to start saving early, whether you currently have children or not. Interest working for you now in a regular savings program is far better than interest working against you in the future in the form of education loans.

Titled for a guy named Coverdell (actually the late Senator Paul Coverdell of Georgia who sponsored the legislation), Coverdell ESAs help families save money for the cost of elementary, high school or higher education for a designated beneficiary. Money grows tax deferred and proceeds can be withdrawn tax-free for qualified education expenses at a qualified institution.

If your modified adjusted gross income is less than $110,000 (or $220,000 if filing a joint return), you may be able to establish a Coverdell ESA. Contributions of up to $2,000 in total can be made per child under the age of 18, no matter how many accounts have been established. Only cash can be contributed to a Coverdell ESA and the contributions must stop after the individual turns 18, unless he/she is a special needs beneficiary. The deadline to open and fund a Coverdell ESA is April 15th for any tax year.

Here are some of the qualified education expenses a Coverdell plan:

Tuition and fees

Books, supplies, and equipment

Academic tutoring

Special needs services for a special needs beneficiary

Room and board

Uniforms

Transportation

Not to confuse things, but many of you may have heard about a 529 plan, which is also a popular investment vehicle to save for your child’s education. The main difference between a Coverdell ESA and a 529 plan is the way you invest the money. With an ESA, you can choose almost any kind of option—stocks, bonds, mutual funds. You can't do that with a 529 and assets in that plan can be used only for higher education.

To learn more and get started on a Firstrade Coverdell ESA, click here to apply.

International Account Holders Can Now Enjoy Unlimited Fund Transfers For Free.

Did you know that you can transfer funds to and from Firstrade for free using ACH, even if you live outside the U.S.?

If you have a U.S. bank account, you can now link it to your Firstrade account to set up online ACH Fund transfers. Once you complete the setup, you can enjoy unlimited fund transfers, without fees or restrictions.

Did you know that you can transfer funds to and from Firstrade for free using ACH, even if you live outside the U.S.?

If you have a U.S. bank account, you can now link it to your Firstrade account to set up online ACH Fund transfers. Once you complete the setup, you can enjoy unlimited fund transfers, without fees or restrictions.

Here’s how it works:

On your desktop computer:

1. Log in to your Firstrade account, go to My Accounts > Deposit/Transfer, click Bank Profile and Setup a Bank Profile

2. Request a verification code through text or email.

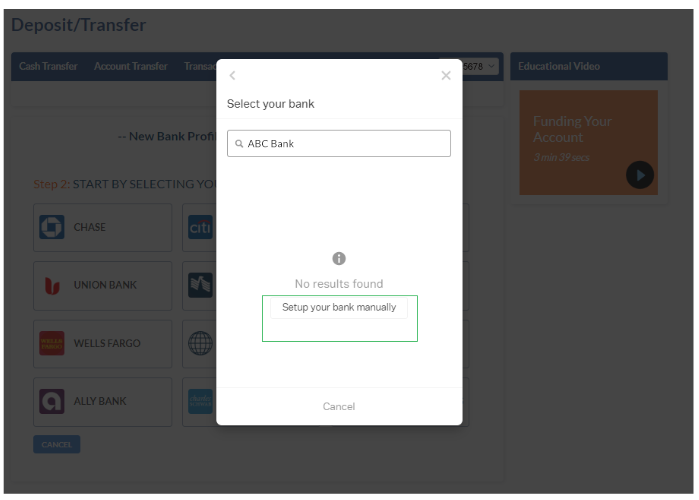

3. Select your bank and link it to your Firstrade account. (If you cannot find your bank on the initial screen, please click on Search for more banks.)

4. If you don’t see your bank on the list, you may link it to Firstrade manually.

5. Fill in your bank information

6. Confirm your bank information and click Submit.

7. Firstrade will send two micro deposits to your bank account within 2 business days. Be sure to return to this page within 10 calendar days to confirm your ACH bank profile.

8. Congratulations, you’re all set!

3 Tips For Managing Traditional and Roth IRA Tax Implications

IRAs and Roth IRAs offer tax advantages that allow you to save more and give Uncle Sam less over time, but certain actions can trigger major tax bills in a given year. If you have either of these retirement accounts, here’s how to get the most out of them and prepare for any related personal income taxes that you might owe this year.

IRAs and Roth IRAs offer tax advantages that allow you to save more and give Uncle Sam less over time, but certain actions can trigger major tax bills in a given year. If you have either of these retirement accounts, here’s how to get the most out of them and prepare for any related personal income taxes that you might owe this year.

Maximize Contributions Before Filing Taxes

To get the most benefit from your IRA or Roth IRA, make sure you contribute the full amount that you’re allowed to. The contribution limit for 2019 is $6,000 for people under 50 years old and $7,000 for seniors age 50 or older. This is an individual limit, so spouses can each have their own account and contribute the maximum allowed.

Moreover, these contributions don’t have to be made by the end of the calendar year. As long as you make contributions before filing your 2019 personal income taxes, those contributions can be counted on your return. The deadline for filing this year is April 15, 2020.

Plan for Taxed Roth IRA Contributions

While Traditional IRA contributions are tax-deductible and will lower how much you owe for the year’s income taxes, the same isn’t true for Roth IRA contributions. Whereas contributions made to Traditionals are pre-tax, anything put in a Roth is post-tax income. As a result, you’ll have to pay income taxes on contributions made to a Roth if you haven’t already.

For some people, this is a moot point because contributions are made from paychecks that have already had income tax withheld. If you’re self-employed or use a non-salary/wage income for these contributions, though, make sure you keep enough to pay the income taxes that will be due.

Reserve Some Withdrawals for Taxes and Penalties

Neither IRA or Roth IRA accounts are intended to have money taken out of them before age 59-1/2 , but you can access the funds in your account should you need to for an emergency. For

example, sometimes people make early withdrawals to avoid bankruptcy, prevent foreclosure or pay unexpected medical bills.

Should you take an early withdrawal, you might be hit with a substantial income tax and penalty depending on how much and what exactly you take out. The implications are as follows:

Early withdrawals from Traditional IRAs are taxed at your income tax rate and assessed a 10-percent penalty.

Withdrawn earnings from Roth IRAs are taxed at your income tax rate and assessed a 10-percent penalty.

Withdrawn contributions from Roth IRAs aren’t taxed or penalized, because you’ve already paid income tax on this money.

Because withdrawals are usually made for financial emergencies, they’re frequently substantial. If you made an early withdrawal this year, reserve some of the funds to pay any taxes and penalties that you need to.

Time is Running Out: Make Your 2019 IRA Contribution

With Tax Day-- April 15-- rapidly approaching, there’s still time to lower your taxable income and save for your retirement as well with a Firstrade no-fee traditional or Roth IRA. A win-win, as they say.

With Tax Day-- April 15-- rapidly approaching, there’s still time to lower your taxable income and save for your retirement as well with a Firstrade no-fee traditional or Roth IRA. A win-win, as they say.

If you already have a Firstrade Traditional or Roth IRA, good for you! You already know all about the great value of IRA investing. But don’t forget, you’ll still eligible to take advantage of 2019 tax benefits by making additional contributions to your IRA before April 15, 2020. You can log in now to start your contribution. (If you’re age 50 or under, you can contribute up to $6,000, and $7,000 if you are age 50 or older.)

If you don’t have an IRA, now’s the time to get started to reduce your taxable income for 2019 and save for your retirement. And best of all, Firstrade’s no-fee IRAs mean that all the money you contribute begins working for you immediately. Don’t delay, to open your no-fee IRA, go here for the application.

2019 and 2020 IRA Contribution Limits and Deadlines:

*You can also make an additional early contribution now for the 2020 tax year.

We’ll be talking more about the many tax benefits of an IRA in an upcoming blog. Stay tuned.