Why the Fed Held Rates Steady in 2026 —and What Sticky Inflation Means for Long-Term Investors

The Fed's 2026 Rate Stance at a Glance

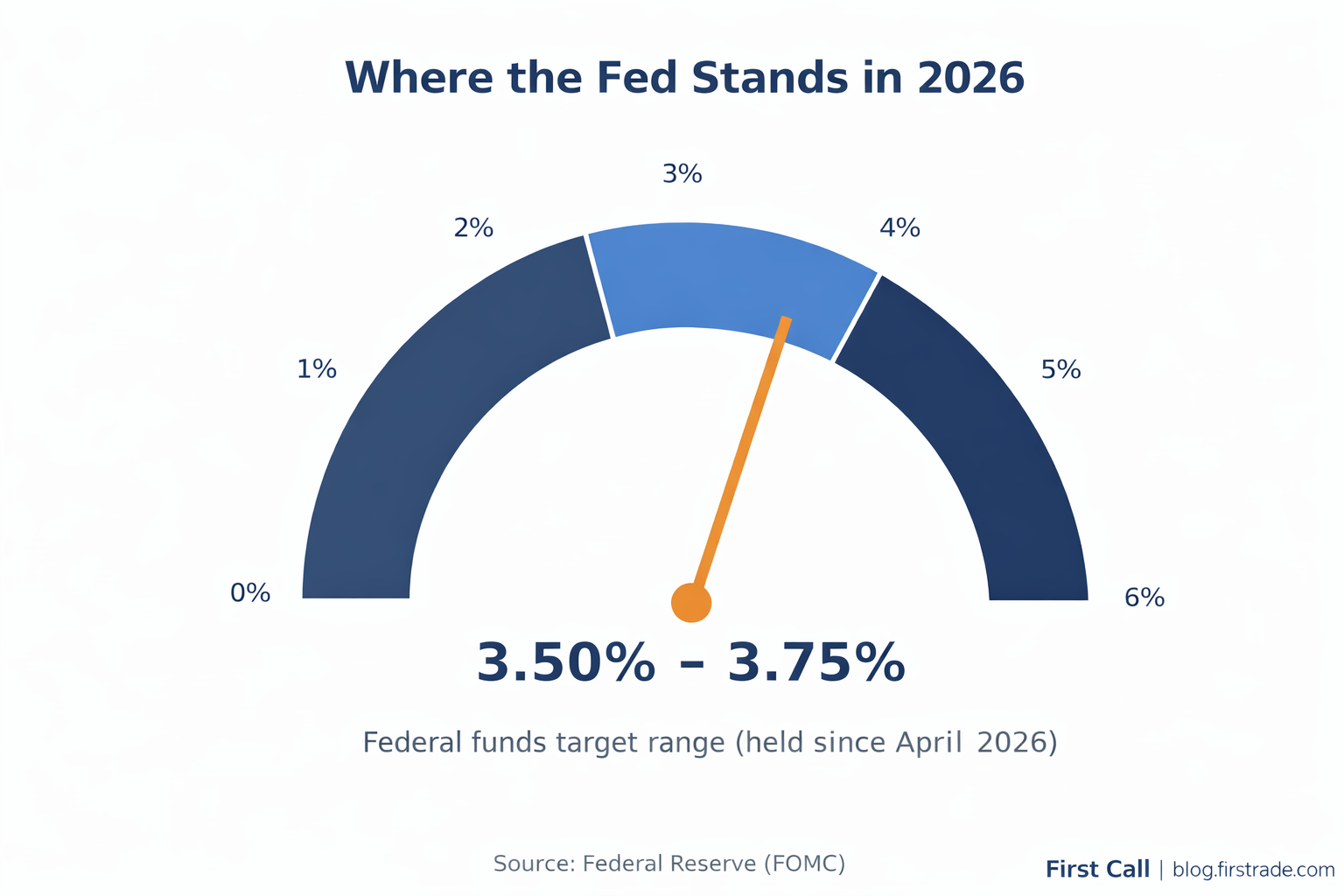

The Federal Reserve's interest rate decision has dominated headlines heading into the June 16–17, 2026 meeting of the Federal Open Market Committee (FOMC). After holding the federal funds target range at 3.50%–3.75% in April, policymakers are widely expected by markets to stay on hold again. For long-term investors, the more important story is not any single meeting but why the Fed is pausing — and how renewed, "sticky" inflation reshapes the case for a diversified, patient approach.

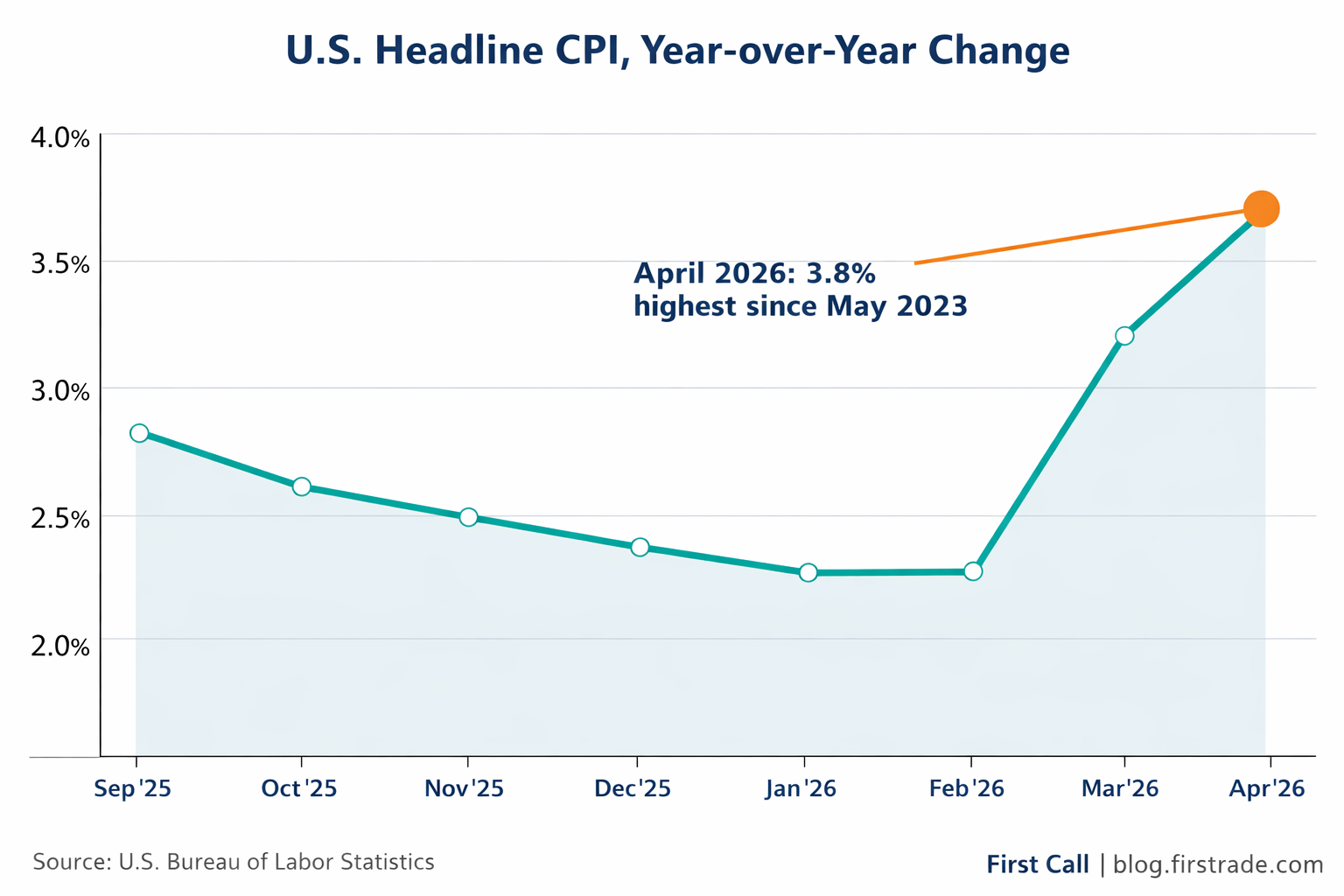

Headline consumer prices rose 3.8% year-over-year in April 2026, according to the U.S. Bureau of Labor Statistics — the fastest pace since May 2023. That figure marks a sharp reversal from the 2.4% readings seen at the start of the year, driven largely by a surge in energy costs tied to geopolitical tensions. With inflation drifting away from the Fed's 2% goal, the central bank has little room to cut rates even as growth moderates.

Headline CPI cooled through early 2026 before re-accelerating to 3.8% in April. Source: U.S. Bureau of Labor Statistics.

Why "Sticky" Inflation Changes the Calculus

Economists describe inflation as "sticky" when price pressures prove slow to fade, often because they are embedded in services, wages, and shelter rather than one-off goods. When inflation is sticky, the Fed typically keeps policy restrictive for longer to avoid letting expectations drift higher. That is the environment investors now face: a labor market still adding jobs — May nonfarm payrolls rose by roughly 172,000 with unemployment near 4.3% (Source: U.S. Bureau of Labor Statistics) — alongside firm prices that argue against near-term cuts.

A new Fed chair, Kevin Warsh, took the helm in May 2026 and inherited a divided committee. While leadership transitions can introduce uncertainty about the policy path, market-implied odds continue to point to no change at the June meeting. The practical takeaway for savers is that borrowing costs and yields on cash and bonds may stay elevated for some time.

The federal funds target range has held at 3.50%–3.75% since April 2026. Source: Federal Reserve (FOMC).

What Higher-for-Longer Rates Mean for a Portfolio

When rates hold steady at restrictive levels, different asset classes respond differently. Cash and short-term Treasury instruments can offer attractive yields, but their purchasing power erodes if inflation outpaces them. Longer-dated bonds carry more price sensitivity to rate expectations. Equities, historically, have tended to reward investors who stay invested across full market cycles, even though individual years can be volatile.

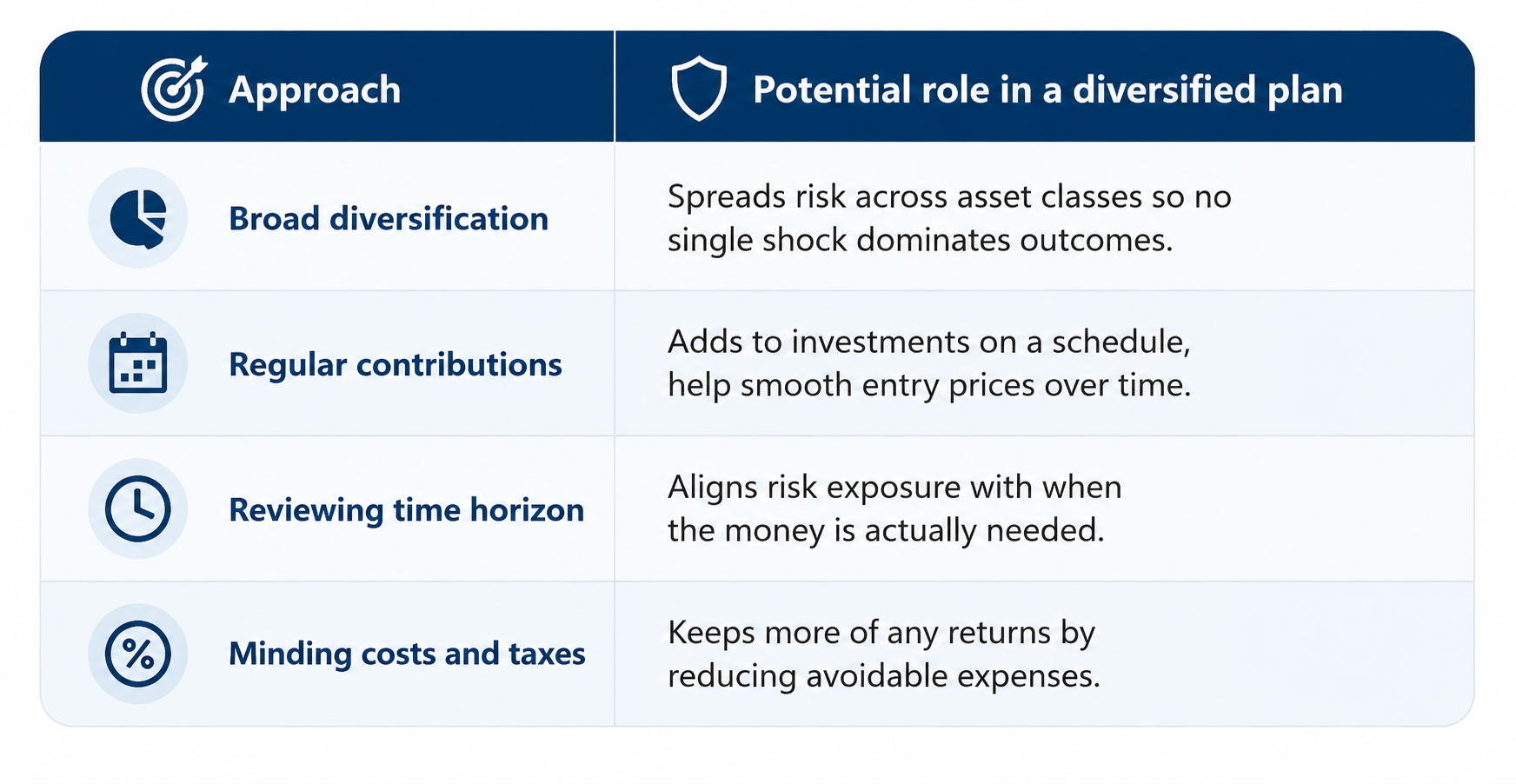

Rather than reacting to a single data point, long-term investors often focus on factors within their control: diversification across asset classes, consistent contributions, a time horizon matched to their goals, and attention to fees and taxes. These principles are educational guideposts, not predictions about where any market will go next.

How Investors Build Inflation Resilience in an Inflation-Affected Market

Frequently Asked Questions

Will the Fed cut interest rates in 2026?

As of early June 2026, markets broadly expect the Fed to hold the federal funds rate at 3.50%–3.75% at the June meeting. With inflation re-accelerating to 3.8% (Source: U.S. Bureau of Labor Statistics, Consumer Price Index, April 2026, released May 2026) the bar for near-term cuts has risen. The actual path will depend on incoming inflation and employment data.

How does inflation affect long-term investors?

Inflation reduces the purchasing power of money over time, which is why many long-term investors hold a diversified mix of investments seeking growth to outpace inflation. Sticky inflation can keep interest rates elevated, affecting both bond yields and the cost of borrowing.

What should investors watch next?

Key data points include the monthly CPI report from the Bureau of Labor Statistics, the FOMC statement and projections, and employment figures. These releases shape expectations for the rate path more than any single forecast.

Important Information: This article is published by First Call (blog.firstrade.com) for educational and informational purposes only. It does not constitute investment, tax, or legal advice, and it is not a recommendation to buy or sell any security. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Figures cited reflect data available as of the publication date and are subject to change. Please consult a qualified professional regarding your individual situation. Securities products and services are offered through Firstrade Securities Inc., Member FINRA/SIPC.