Your 2026 Retirement Savings Playbook: New IRA and 401(k) Limits Explained

Every year, the IRS adjusts retirement account contribution limits to keep pace with inflation—and 2026 brings meaningful increases that could help you build wealth faster. Whether you’re just starting your retirement journey or fine-tuning a decades-long strategy, understanding the new numbers and rules is essential. In this guide, we’ll walk through the updated 2026 IRA and 401(k) limits, key rule changes for high earners, and practical strategies to make the most of your retirement savings.

2026 Contribution Limits at a Glance

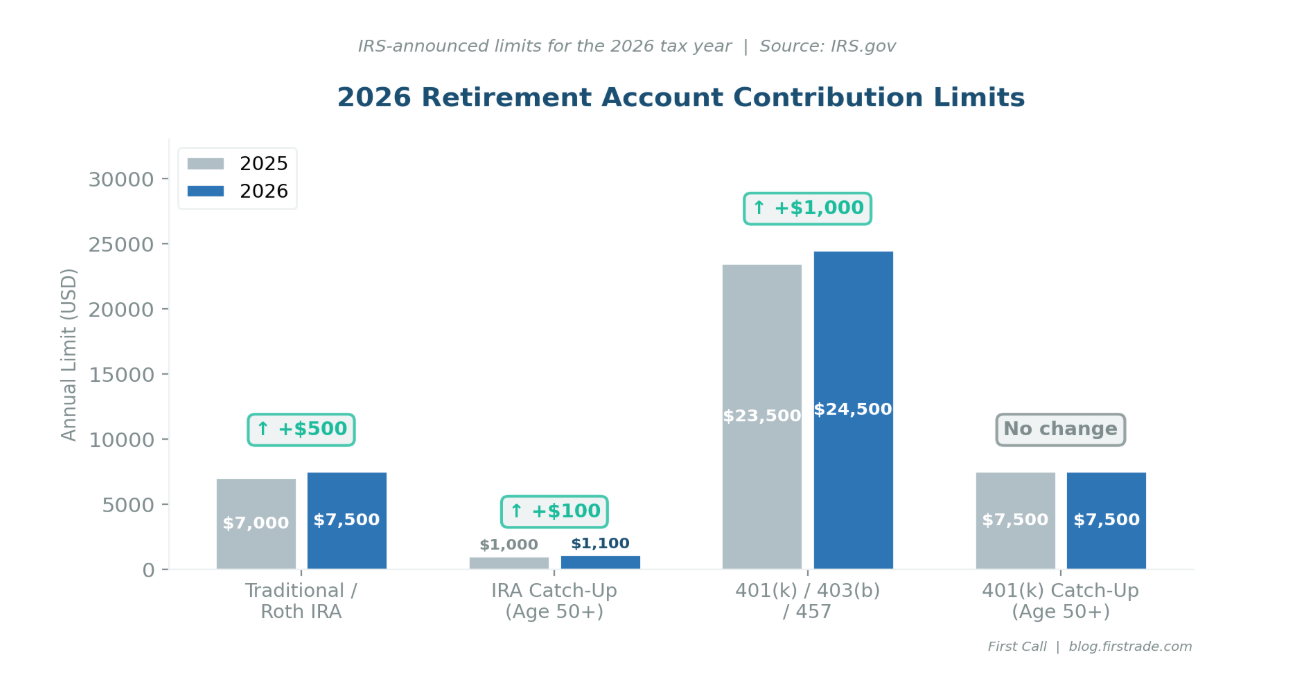

The IRS has announced the following increases for the 2026 tax year:

Figure 1: Side-by-side comparison of 2025 vs. 2026 retirement account contribution limits.

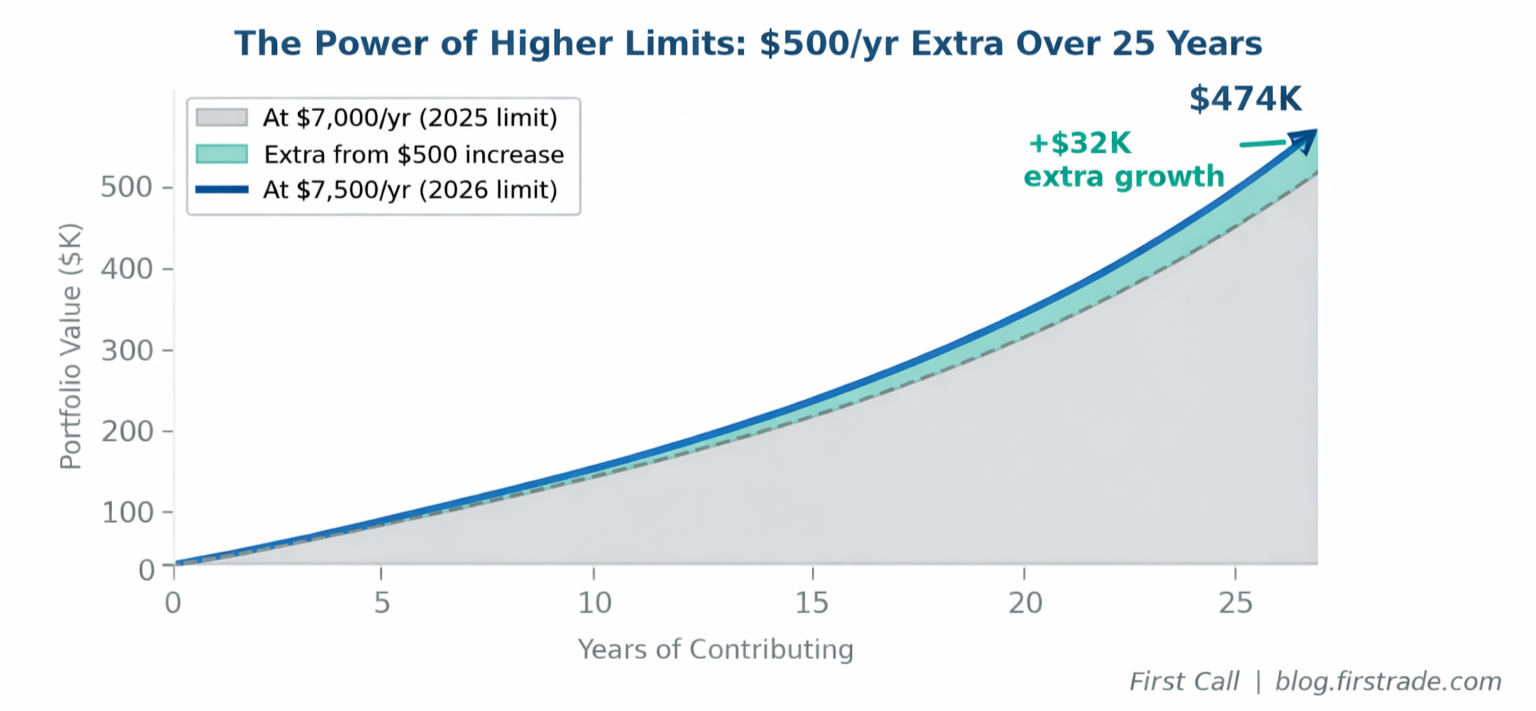

These may seem like modest increases individually, but compounded over years of investing, even an extra $500 per year can grow into a meaningful sum.

Figure 2: An extra $500/year at 7% return grows to approximately $32,000 in additional growth over 25 years. For illustrative purposes only and does not represent a real investment as rates of return will vary over time and loss of principal is possible.

New Roth Catch-Up Rule: What Higher Earners Need to Know

One of the most significant changes for 2026 affects higher-income earners making catch-up contributions to employer-sponsored plans like 401(k)s. Starting this year, if your FICA wages exceeded $145,000 in the previous year, all catch-up contributions must be designated as Roth (after-tax) contributions rather than pre-tax.

What does this mean in practice?

You’ll pay taxes on catch-up contributions now, but withdrawals in retirement will be tax-free.

This effectively creates a forced Roth savings vehicle for higher earners—which can be advantageous if tax rates rise in the future.

Check with your plan administrator to ensure your account accepts Roth catch-up contributions.

Roth IRA Income Phase-Outs: Am I Eligible?

Direct Roth IRA contributions remain subject to income limits. For 2026, single filers can contribute the full amount if MAGI is below $153,000 (up from $150,000 in 2025). The phase-out range for married filing jointly also increased.

If your income exceeds these thresholds, the “backdoor Roth IRA” strategy—contributing to a traditional IRA and then converting to a Roth—remains available with no income limits on conversions. Consult a tax professional before proceeding.

Smart Retirement Strategies for Every Life Stage

In Your 20s–30s: Build the Habit

Time is your greatest asset. 77% of Gen Z investors started investing before age 25. Consider starting with a Roth IRA if you’re in a lower tax bracket—your contributions grow and are withdrawn tax-free in retirement*.

In Your 40s–50s: Optimize and Maximize

Push contributions toward the maximum. With the 2026 401(k) limit at $24,500 and IRA at $7,500, you could shelter over $32,000 per year (or $40,600 with catch-up). Review your asset allocation and consider whether a Roth conversion makes sense.

In Your 60s and Beyond: Strategize Distributions

Strategic Roth conversions can be particularly effective between retirement and required minimum distributions, especially during market drawdowns. There are no income limits on conversions, and paying conversion tax from outside cash preserves your invested balance.

How to Put These Strategies Into Action

With a self-directed brokerage like Firstrade, you can open Traditional IRAs, Roth IRAs, and rollover accounts with commission-free trading across stocks, ETFs, options, and mutual funds—giving you the flexibility to implement your own retirement strategy.

The Bottom Line

The 2026 retirement savings landscape brings higher limits, new Roth rules, and continued opportunities for tax-efficient wealth building. Every dollar invested today is working for your future self. At Firstrade, we’re here to help you invest with confidence.

This article is for educational and informational purposes only and does not constitute investment, tax, or legal advice. Tax laws and retirement account rules are complex and subject to change. Please consult a qualified tax professional or financial advisor. All investments involve risk, including loss of principal. Firstrade Securities Inc. is a member of FINRA/SIPC. *Subject to certain restrictions. Please consult with your tax advisor. Firstrade Securities does not provide tax or legal advice.