The $700 Billion AI Infrastructure Boom: What Retail Investors Should Know

The artificial intelligence investment wave has reached a scale that is difficult to overstate. In 2026, the five largest U.S. cloud and AI infrastructure providers — Amazon, Alphabet, Microsoft, Meta, and Oracle — have collectively committed to spending between $660 billion and $700 billion on capital expenditure, nearly doubling their 2025 levels. This unprecedented spending spree is reshaping the semiconductor industry, driving record demand for memory chips, and creating both opportunities and risks for retail investors trying to navigate the AI supercycle.

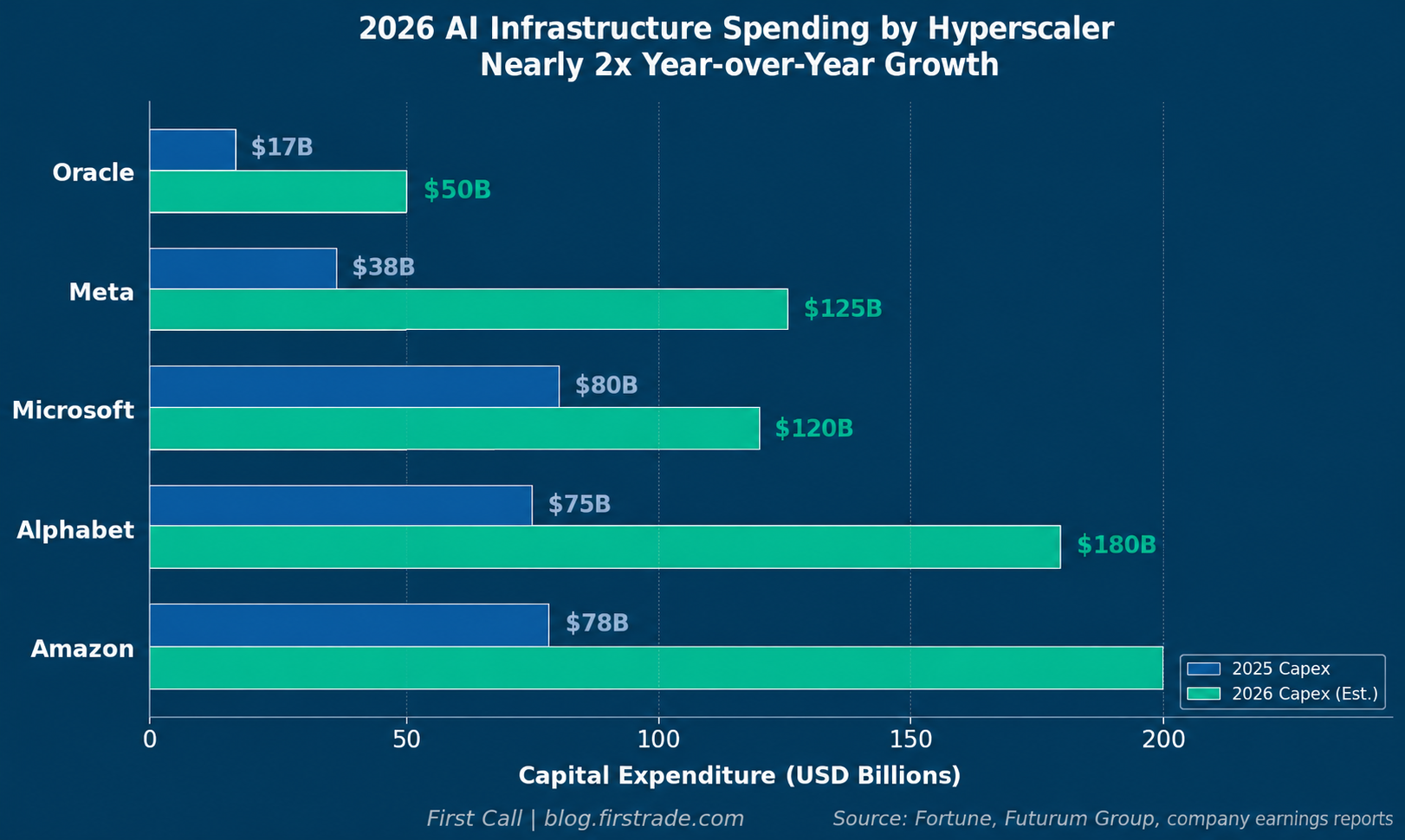

How Much Are the Hyperscalers Spending on AI?

The numbers are staggering. Amazon leads the pack with a projected $200 billion in 2026 capital expenditure, followed by Alphabet at $175–185 billion, Meta at $115–135 billion, Microsoft tracking toward $120 billion or more, and Oracle targeting $50 billion. To put this in perspective, the combined AI infrastructure budget of these five companies is roughly 77% above last year’s already-record levels, and it exceeds the GDP of most countries.

This spending is going toward building data centers, purchasing AI accelerator chips (primarily from NVIDIA), expanding networking infrastructure, and securing the enormous power capacity needed to run AI workloads. The scale of investment reflects the hyperscalers’ conviction that AI will be the dominant growth driver of the next decade — and their fear of falling behind competitors in the race to build AI infrastructure.

Why Are Memory Chips at the Center of the AI Boom?

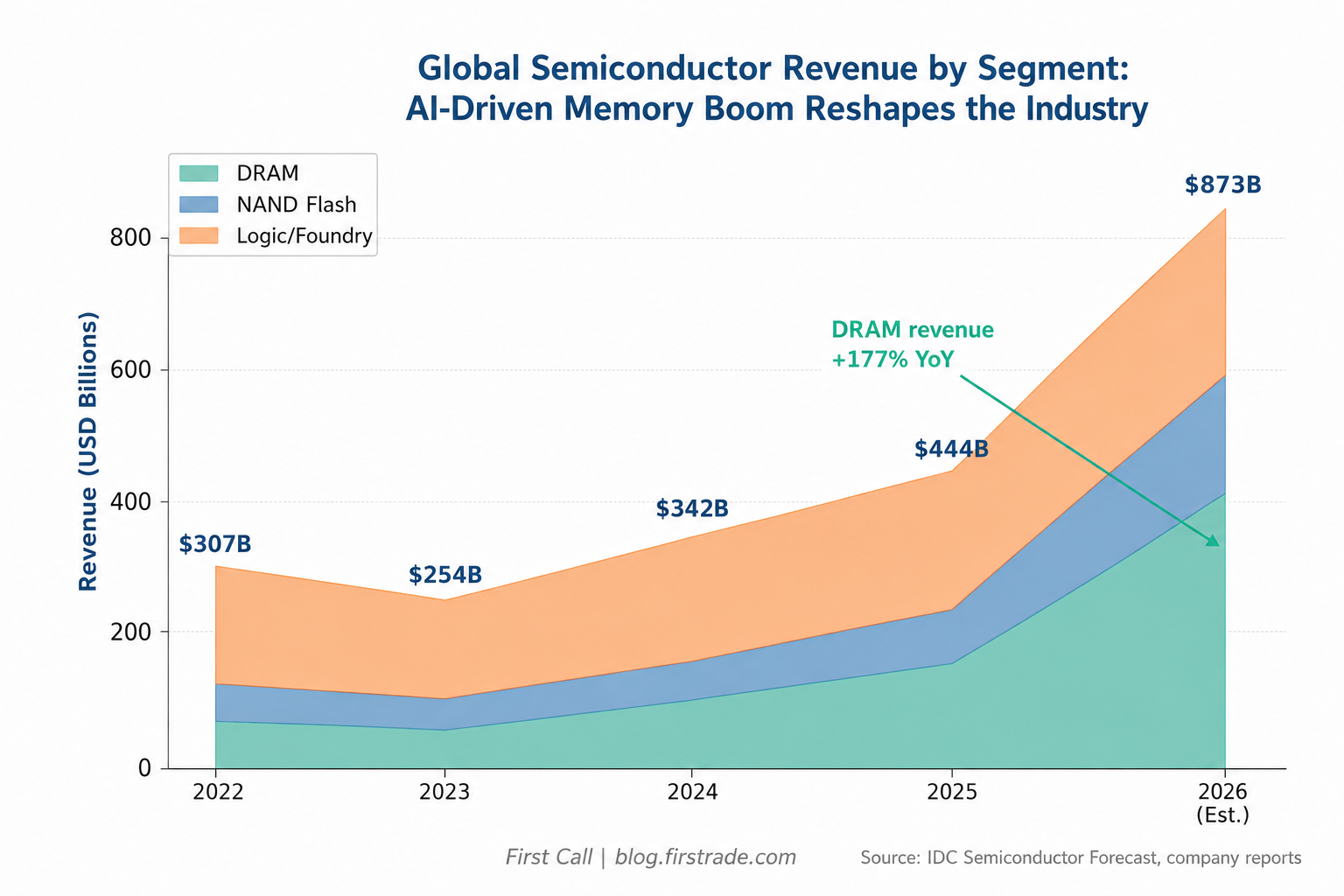

High-bandwidth memory (HBM) has emerged as the critical bottleneck in the AI hardware supply chain. Every AI accelerator chip requires large amounts of fast memory to process the massive datasets used in training and running AI models. This has created an extraordinary demand surge for DRAM and NAND Flash memory.

According to IDC, DRAM revenues are forecast to reach $418.6 billion in 2026, up 177% year over year. NAND Flash revenues are projected at $174.1 billion, up 138.5% from 2025. Most high-bandwidth memory capacity is already pre-committed through 2026, with forward allocations extending into 2027 — a level of demand visibility that is virtually unprecedented in the semiconductor industry.

The market has taken notice. The Roundhill Memory ETF (DRAM) soared nearly 30% in just one week, and the broader semiconductor sector now sits at the largest weight in the S&P 500 of any sector.

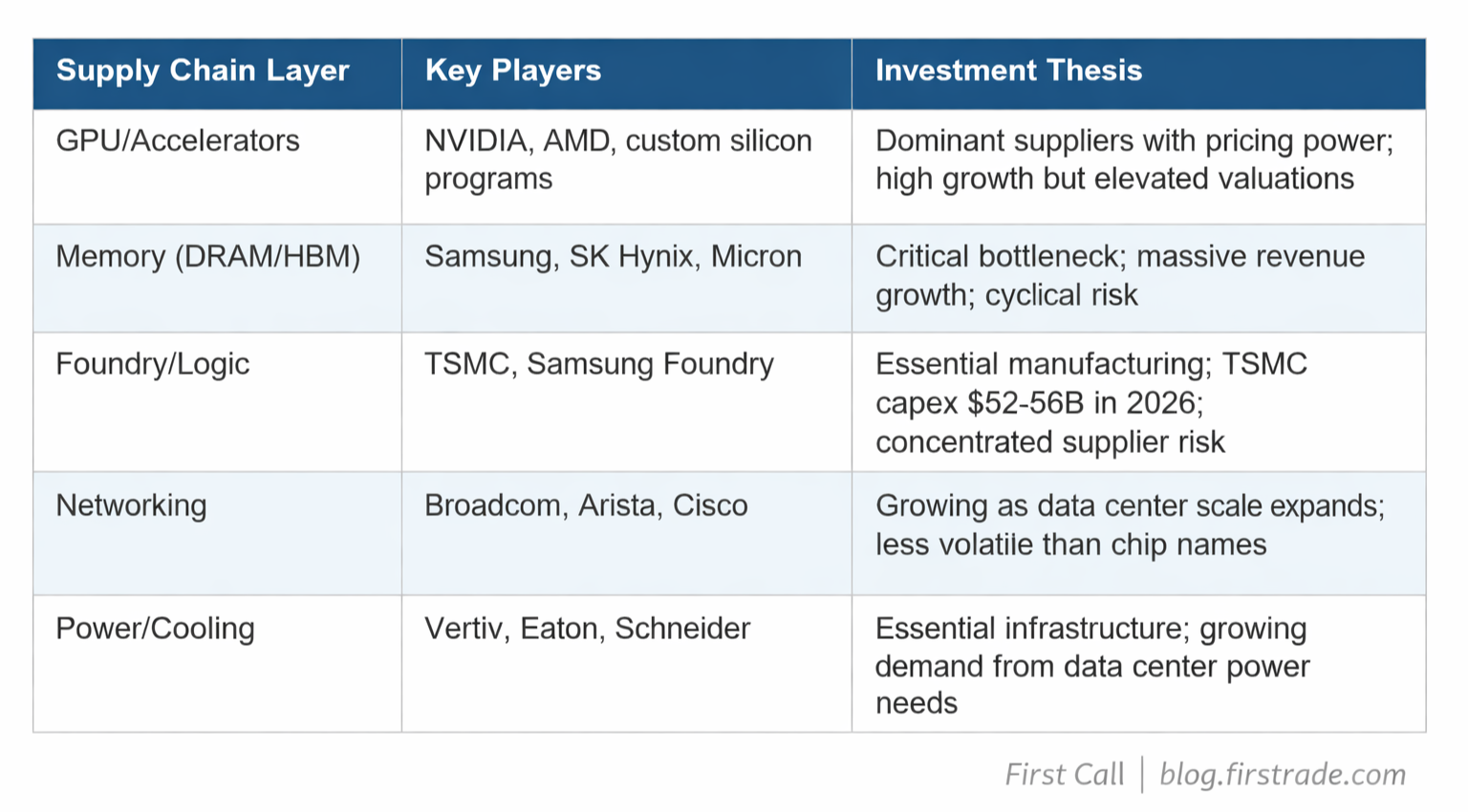

Where Is the Money Flowing in the AI Supply Chain?

Understanding the AI infrastructure supply chain can help investors identify where value is being created. The spending flows through several layers, each with distinct investment characteristics.

What Are the Risks of Investing in the AI Theme?

Despite the extraordinary growth, the AI infrastructure trade carries real risks that investors should understand before committing capital.

Valuation risk: Many AI-related stocks are trading at historically elevated multiples. If earnings growth disappoints even slightly, the downside could be significant.

Cyclicality: The semiconductor industry has a long history of boom-and-bust cycles. Current demand levels are unprecedented, but the supply chain is adding capacity that could lead to oversupply in 2027–2028.

Concentration risk: A significant portion of AI hardware revenue flows through a handful of companies, particularly NVIDIA and TSMC. Any disruption to these suppliers could have outsized market impact.

Geopolitical risk: Taiwan’s role in semiconductor manufacturing and ongoing trade tensions between the U.S. and China add a layer of geopolitical uncertainty to the AI supply chain.

Return on investment uncertainty: While hyperscalers are spending record amounts, the question of whether AI will generate sufficient returns to justify $700 billion in annual infrastructure investment remains open.

How Can Retail Investors Participate Thoughtfully?

For investors who want exposure to the AI infrastructure theme without concentrating risk in a single stock, several approaches are worth considering. Diversified semiconductor ETFs provide broad exposure across the supply chain. Allocating across multiple layers — chips, memory, networking, and power infrastructure — can reduce company-specific risk. Dollar-cost averaging into positions rather than making large lump-sum bets can help manage timing risk in a volatile sector.

Perhaps most importantly, investors should size their AI-related positions appropriately within their overall portfolio. The semiconductor sector’s growing weight in the S&P 500 means that passive index investors already have significant AI exposure. Adding concentrated bets on top of existing index holdings can create unintended overexposure to a single theme.

The Bottom Line

The $700 billion AI infrastructure boom represents one of the largest capital expenditure cycles in corporate history. For retail investors, it offers genuine opportunities — but those opportunities come with elevated valuations, cyclical risks, and concentration concerns that demand careful portfolio management. The AI supercycle is real, but investing wisely in it requires looking beyond the headlines to understand where value is being created, where risks are accumulating, and how much exposure is appropriate for your individual financial goals.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Consult a qualified financial advisor before making any investment decisions. Firstrade Securities Inc. is a member of FINRA/SIPC. Any references to specific companies are for illustrative purposes only and not a recommendation to buy or sell any specific securities.