What Rising Treasury Yields Mean for Everyday Investors in 2026

Why Treasury Yields Are in the Spotlight

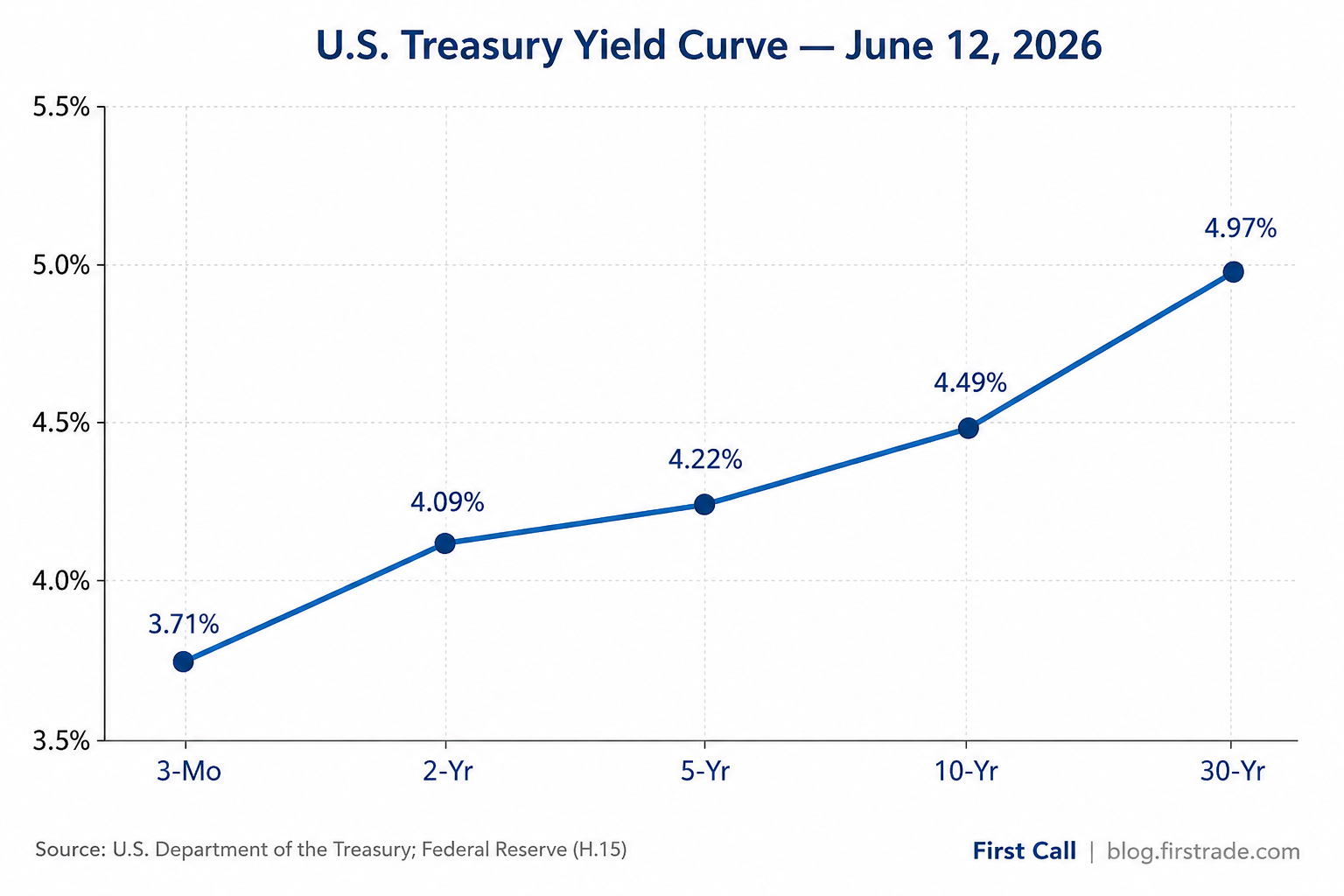

Rising Treasury yields have become one of the defining stories for investors in 2026. As of June 12, 2026, the 10-year Treasury note yielded about 4.49% and the 30-year bond reached roughly 4.97%, according to the U.S. Department of the Treasury and the Federal Reserve's H.15 release. Shorter maturities also climbed, with the 2-year note near 4.09% — among its highest readings in over a year. For everyday investors, these moves influence everything from savings yields to bond returns to the cost of borrowing.

Yields rose as markets weighed escalating geopolitical tensions in the Middle East and a firmer reading on wholesale prices. After a strong 2025, bonds saw renewed volatility in early 2026 as Treasury rates broke out of their prior trading range. The upside for savers is that higher starting yields can provide a stronger foundation for future income — though prices can still move as conditions change.

The U.S. Treasury yield curve sloped upward across maturities on June 12, 2026. Source: U.S. Department of the Treasury; Federal Reserve (H.15).

Understanding the Treasury Yield Curve

The yield curve plots interest rates across maturities, from short-term Treasury bills to 30-year bonds. When longer maturities yield more than shorter ones — as they did in mid-June 2026 — the curve is described as upward-sloping, a shape often associated with expectations of steady growth and persistent inflation. The curve matters because it serves as a benchmark for mortgages, corporate borrowing, and the pricing of many other investments.

A key relationship every investor should understand is that bond prices and yields move in opposite directions. When yields rise, the market price of existing bonds generally falls; when yields decline, existing bond prices tend to rise. This is why longer-dated bonds, which lock in a rate for many years, can be more sensitive to changing yields than short-term instruments.

Where Cash Fits: Money Market Funds and T-Bills

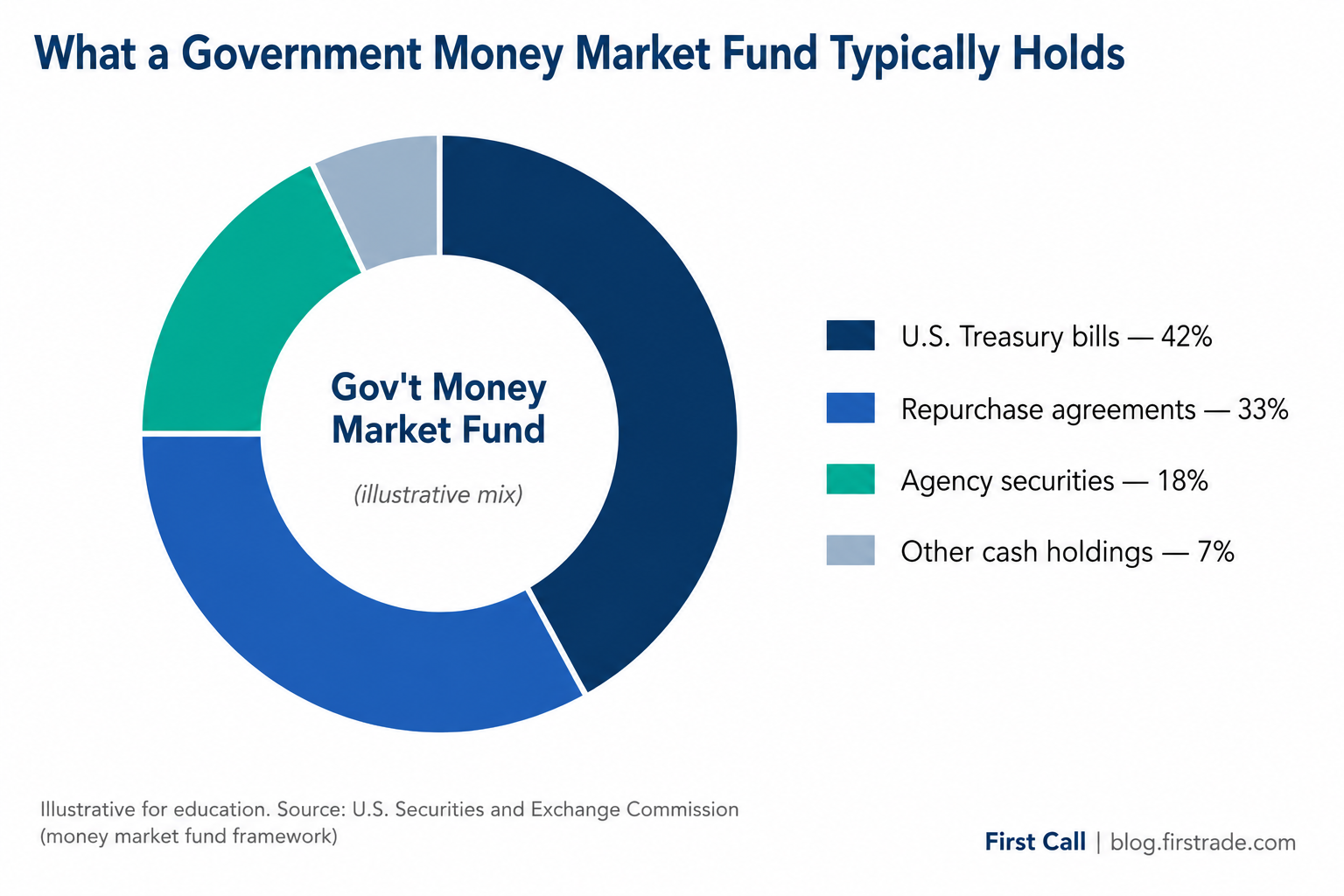

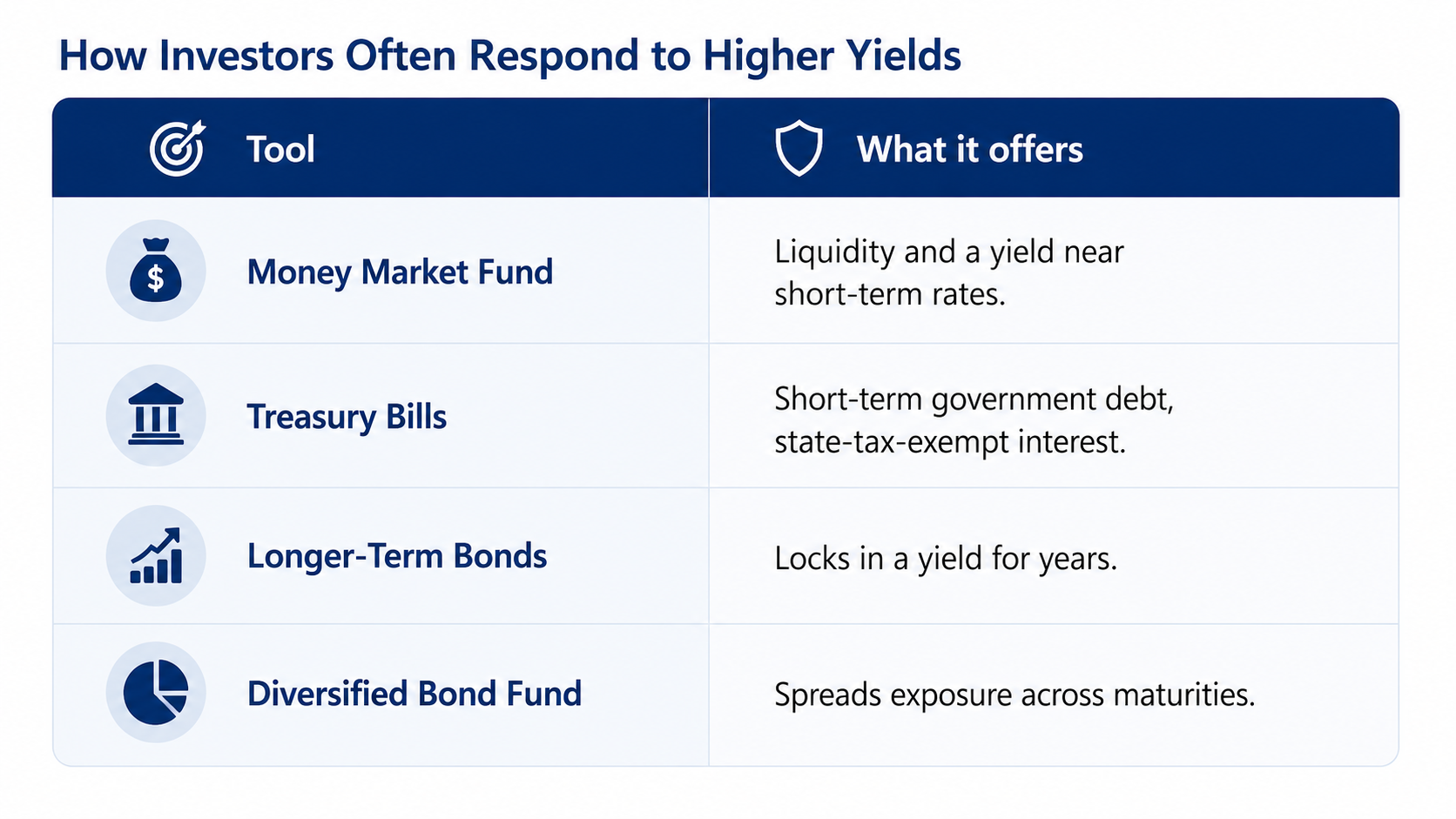

Higher short-term yields have renewed interest in cash-like options. A government money market fund holds very short-term, high-quality debt — such as Treasury bills, agency securities, and repurchase agreements — and aims for liquidity, principal stability, and a yield that tracks short-term rates. Many investors pair a brokerage cash position with such a fund to earn near-policy yields while keeping money accessible.

A government money market fund typically holds Treasury bills, repos, and agency securities (illustrative). Source: U.S. Securities and Exchange Commission framework.

Treasury bills purchased directly are another way investors hold short-term government debt, with interest exempt from state and local income tax. The right mix of cash, bills, and longer bonds depends on an investor's time horizon, liquidity needs, and tolerance for price swings — not on any single yield reading.

Access matters too. Through Firstrade, investors can buy U.S. Treasury bills, notes, and bonds directly inside a brokerage account, with Treasuries offered on a net yield basis and no separate trading commission. The same account also provides municipal bonds, agency bonds, and CDs for those building a fixed-income ladder, alongside commission-free trading in stocks, ETFs, options, and mutual funds. With web and mobile platforms plus built-in research, an investor can keep short-term cash positions and longer-term holdings in one place — though, as always, which investments fit depends on individual goals rather than any single platform feature.

Frequently Asked Questions

Why do bond prices fall when yields rise?

Bond prices and yields move inversely. When new bonds are issued at higher yields, existing bonds paying lower rates become less attractive, so their market price falls until their effective yield is competitive. The longer a bond's maturity, the more its price typically moves for a given change in yields.

Are money market funds the same as savings accounts?

No. A money market fund is an investment product, not a bank deposit, and is not FDIC-insured. Government money market funds aim for stability and liquidity, but their yields move with short-term interest rates and are not guaranteed.

What should investors watch with Treasury yields?

Useful references include the U.S. Treasury's daily par yield curve, the Federal Reserve's H.15 release, and incoming inflation and employment data. These shape the path of yields more reliably than any single forecast.

Disclaimer: This article is published by First Call (blog.firstrade.com) for educational and informational purposes only. It does not constitute investment, tax, or legal advice, and it is not a recommendation to buy or sell any security. Investing involves risk, including the possible loss of principal. Money market funds are not bank deposits and are not FDIC-insured. Past performance does not guarantee future results. Figures cited reflect data available as of the publication date and are subject to change. Please consult a qualified professional regarding your individual situation. Securities products and services are offered through Firstrade Securities Inc., Member FINRA/SIPC.