Tax-Loss Harvesting: A Mid-Year Guide for Investors in 2026

What Is Tax-Loss Harvesting?

Tax-loss harvesting is a strategy in which an investor sells an investment that has dropped in value to realize a capital loss, then uses that loss to offset capital gains elsewhere in a taxable account. According to IRS guidance, realized losses first offset realized gains of the same type, and any excess can offset other gains or a limited amount of ordinary income. The goal is not to lose money on purpose — it is to make productive use of losses that already exist on paper, turning a market dip into a potential tax benefit. This mid-year guide explains how tax-loss harvesting works in 2026, the rules that govern it, and why June can be a smart time to review your portfolio.

It is worth emphasizing at the outset that this strategy applies only to taxable brokerage accounts. Losses inside tax-advantaged accounts such as IRAs and 401(k) plans cannot be harvested, because gains and losses inside those accounts are not taxed year to year.

Why Mid-Year Is a Smart Time to Review

Tax-loss harvesting is most often associated with December, when investors scramble before the year-end deadline. But waiting until December has drawbacks: opportunities that existed earlier in the year may have disappeared, and a crowded year-end can lead to rushed decisions. Reviewing your portfolio at mid-year — around the June 15 deadline for second-quarter estimated taxes — gives you a natural checkpoint to assess unrealized losses while there is still ample time to act thoughtfully. It also spreads the work across the year rather than concentrating it into a single hectic month.

A Simple Example of How It Works

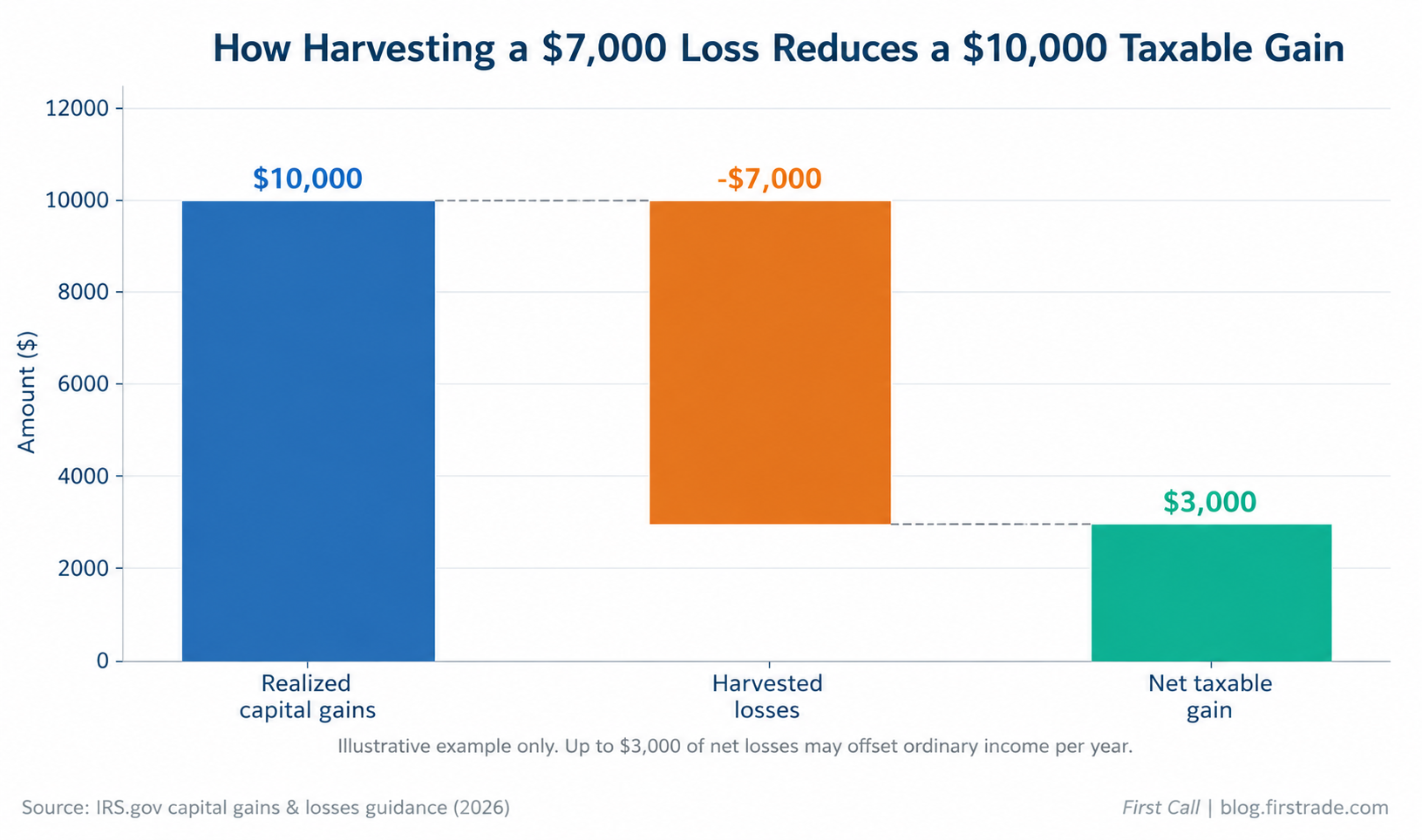

Suppose an investor has realized $10,000 in capital gains earlier in the year. Reviewing the portfolio at mid-year, they identify a separate holding sitting at a $7,000 unrealized loss. By selling that position, they realize the $7,000 loss, which offsets a portion of the gains. The taxable gain falls from $10,000 to $3,000. The investor still made money overall, but the amount exposed to capital gains tax is substantially smaller.

Figure 1. An illustrative example: a $7,000 harvested loss reduces a $10,000 taxable gain to $3,000. For education only. Source: IRS.gov.

This is a simplified illustration. Real situations involve short-term versus long-term classifications, which are taxed at different rates, and the IRS requires that losses offset gains of the same type first. Still, the core idea holds: a realized loss can reduce the gains that would otherwise be taxed.

The Wash-Sale Rule: The 61-Day Trap

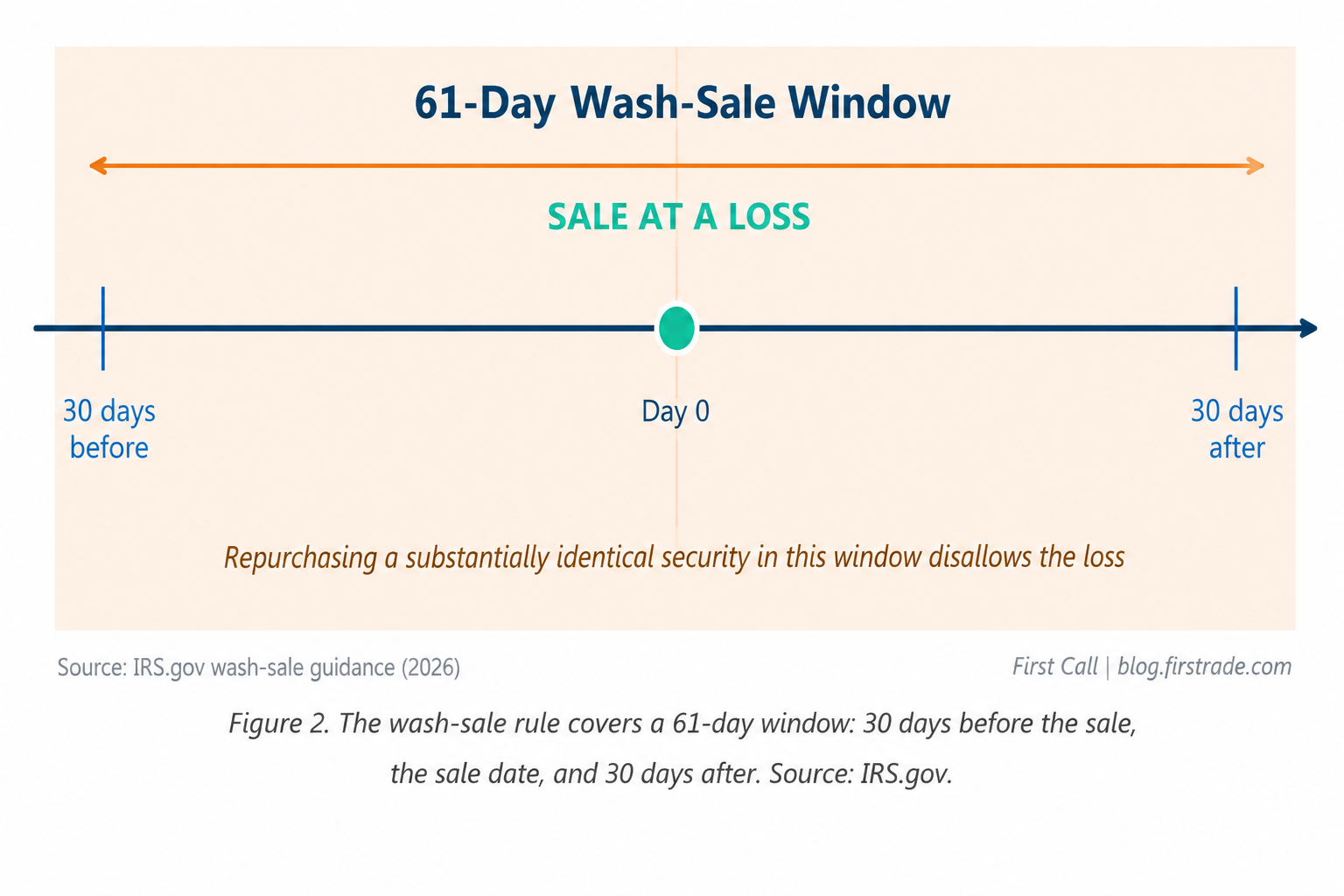

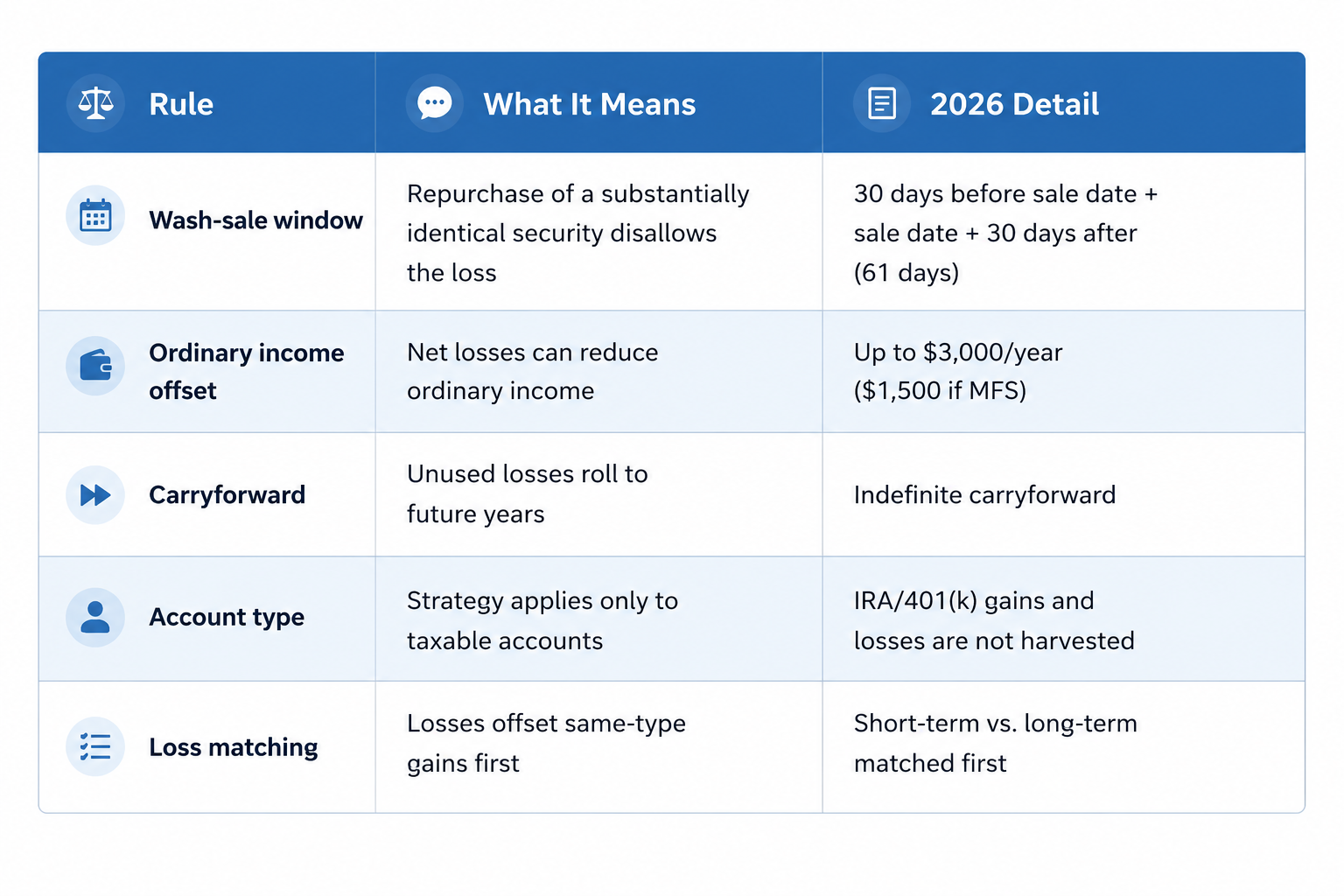

The most important rule to understand is the wash-sale rule. The IRS prohibits claiming a loss if you buy the same security — or one that is “substantially identical” — within 30 days before or after the sale that produced the loss. Counting the sale date itself, that creates a 61-day window in which a repurchase disallows the loss. The disallowed loss is not gone forever; it is generally added to the cost basis of the new shares, but the immediate tax benefit is lost.

Figure 2. The wash-sale rule covers a 61-day window: 30 days before the sale, the sale date, and 30 days after. Source: IRS.gov.

A detail many investors miss: the wash-sale rule applies across all accounts you and your spouse control, including IRAs. Buying a substantially identical security in your IRA shortly after harvesting a loss in your taxable account can still trigger the rule. Careful timing — and choosing a similar but not “substantially identical” replacement — is how investors commonly stay on the right side of this rule while keeping their market exposure roughly intact.

The $3,000 Rule and Carryforwards

What happens if your losses exceed your gains? IRS rules allow net capital losses to offset up to $3,000 of ordinary income per year ($1,500 if married filing separately). Any losses beyond that limit are not wasted — they carry forward to future tax years indefinitely, where they can offset future gains or, again, up to $3,000 of ordinary income each year. This carryforward feature means a large loss harvested today can continue providing tax benefits for years.

Quick Reference: Key Tax-Loss Harvesting Rules

Frequently Asked Questions

Does tax-loss harvesting only work in December?

No. It can be done any time the market provides an opportunity. Reviewing mid-year lets you act on losses before they potentially recover and avoids a rushed year-end scramble.

Can I harvest losses in my IRA or 401(k)?

No. These are tax-advantaged accounts, so gains and losses inside them are not taxed annually. Tax-loss harvesting applies only to taxable brokerage accounts.

What counts as a ‘substantially identical’ security?

The IRS does not publish a precise list, but it generally includes the same stock or a fund that tracks the same index very closely. Many investors replace a harvested holding with a similar — but not identical — investment to avoid triggering the wash-sale rule.

This is not intended to be tax advice, always consult your own tax advisor regarding your own situation.

Important Disclosures

Disclaimer: This article is provided by First Call (blog.firstrade.com) for educational and informational purposes only. It does not constitute investment, tax, or legal advice, and it is not a recommendation to buy or sell any security or to adopt any investment strategy. Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Please consult a qualified financial or tax professional regarding your individual circumstances. Securities products and services are offered through Firstrade Securities Inc., a member of FINRA and SIPC. Brokerage products are not FDIC insured, are not bank guaranteed, and may lose value.